- How It Works

- ServicesServicesOverviewChoose the right level of support for your plan and needsExpert ReviewA comprehensive review of inputs and reports to get you on the right pathFiling AssistanceLet our experts deal with Social Security for youClawback AssistanceFor those who need help fighting a Social Security benefit clawback

- Why Choose Us

- ResourcesResourcesBooksFrom the world-renowned economist behind Maximize My Social SecurityWebinars & PodcastsExpert tips and guides to help you get the maximum from Maximize My Social SecurtyArticlesIn-depth commentary on Social Security from our founderAsk LarryThousands of questions answered by our Social Security expertsBlogSocial Security insights to help you maximize your lifetime benefitsFAQYour most pressing questions answered

- Pricing

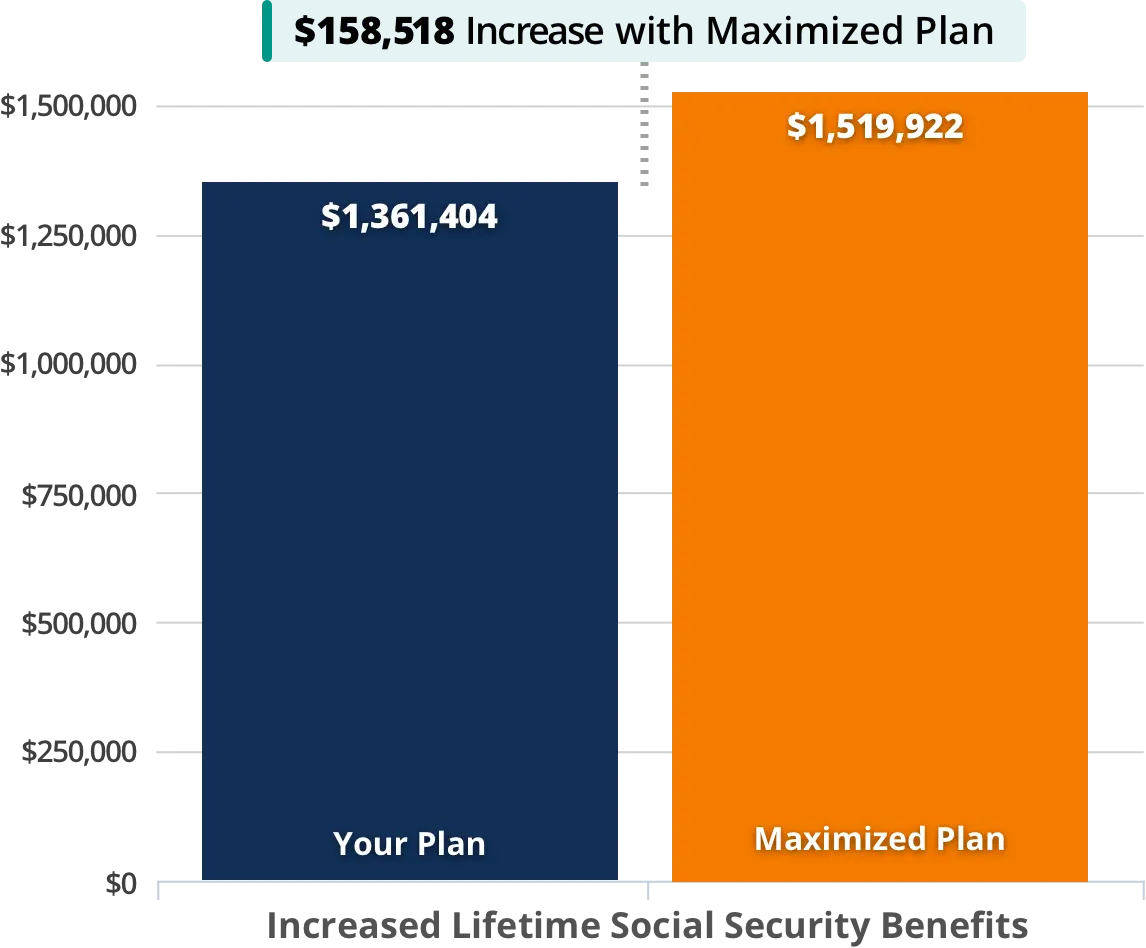

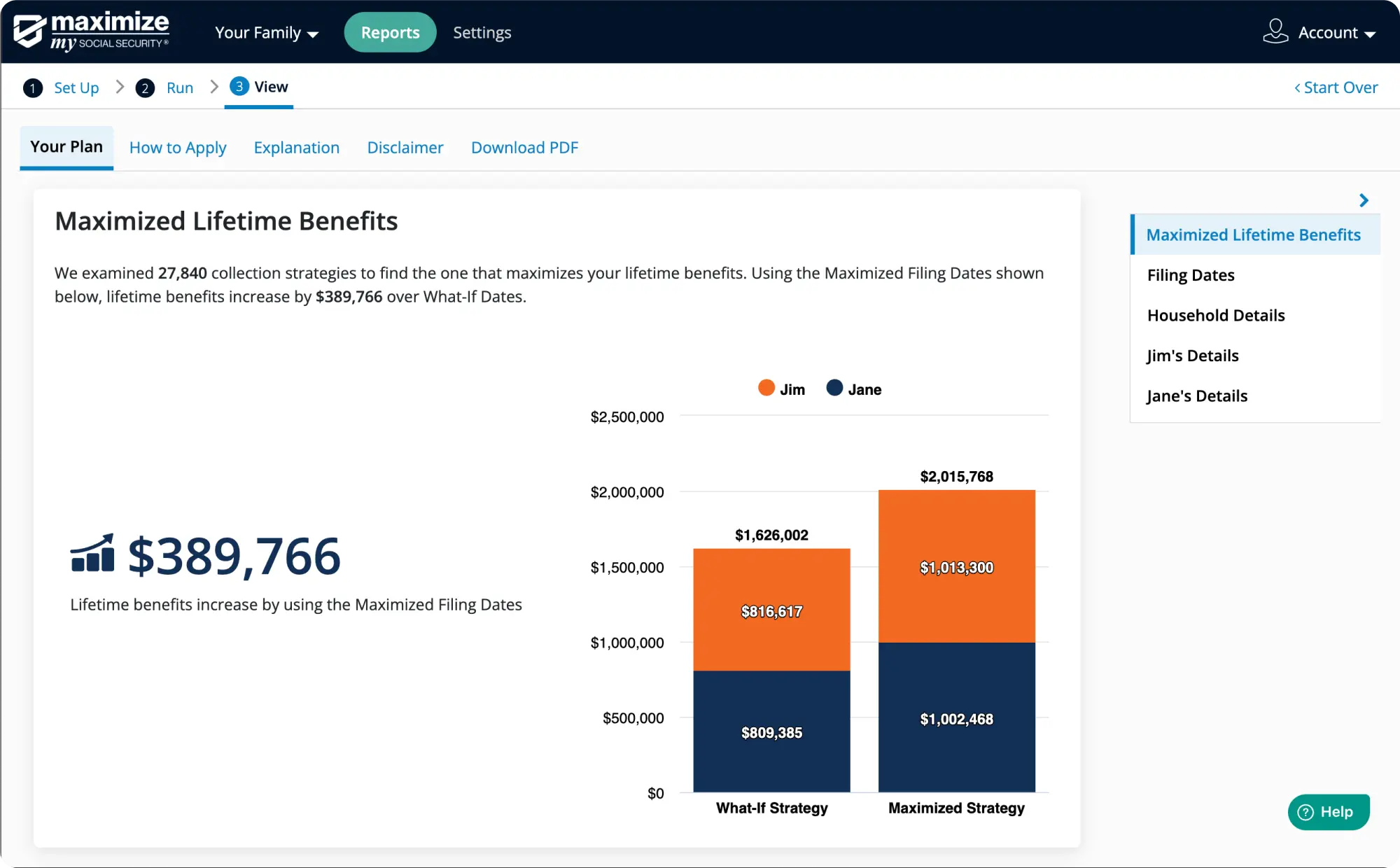

Maximized Benefits with a Clear Plan

Maximize My Social Security handles all the complexity of Social Security's strategies, benefits, and rules. You get a clear roadmap for filing to get the highest possible benefits.

Maximizes Lifetime Social Security Benefits

Our advanced software finds the best strategy to increase lifetime Social Security benefits.

Accurate and comprehensive, our software handles difficult calculations that other calculators don't.

Covers every situation:

Accurate and comprehensive, our software handles difficult calculations that other calculators don't.

Covers every situation:

All possible filing strategies

- Delay retirement to receive higher benefits

- Work longer, earning more to increase benefits

- Continue to be able to file, suspend and reinstate retirement benefits

- Retire early to activate child or disabled-child benefits and child-in-care spousal benefits

- Start widow(er) benefit before full retirement when deceased spouse took retirement benefits early

- Delay retirement benefits to raise widow(er) benefits for surviving spouse or ex-spouse

All major benefits

- Retirement Insurance Benefits

- Spouse's Insurance Benefits

- Divorced Spouse's Insurance Benefits

- Social Security Disability Insurance Benefits

- Child In-Care Spouse's Insurance Benefits

- Widow(er)'s Insurance Benefits

- Divorced Widow(er)'s Insurance Benefits

- Child's Insurance Benefits

- Childhood Disability Benefits

- Surviving Child's Insurance Benefits

- Father's and Mother's Insurance Benefits

All major rules and provisions

- New Social Security laws and grandfathering rules

- Early benefit reductions

- Delayed retirement credits

- The earnings test

- Adjustment of the reduction factor

- Re-computation of benefits

- Option to suspend and reinstate retirement benefits

- Family maximum

- Combined family maximum

- Disabled family benefit maximum

- RIB LIM on widow(er) benefits when deceased spouse claimed early

- Restricted application and deeming rules

- Alternate widow(er)'s benefits when the deceased spouse died before age 62

Cuts the Complexity

Deciding which benefits to take and when is among the most important decisions households make.

Making the right decisions can increase your Social Security benefits by tens to hundreds of thousands of dollars. Making these decisions on your own is virtually impossible.

Why? Because Social Security is incredibly complex.

Social Security benefits are calculated based on thousands of rules and even more complicated rules about those rules.

Our software's expert algorithms find your highest Social Security lifetime benefits.

Making the right decisions can increase your Social Security benefits by tens to hundreds of thousands of dollars. Making these decisions on your own is virtually impossible.

Why? Because Social Security is incredibly complex.

Social Security benefits are calculated based on thousands of rules and even more complicated rules about those rules.

Our software's expert algorithms find your highest Social Security lifetime benefits.

Clear Instructions. Shows How and When to File.

Specific to-do list for all plans

- Actions to take

- Filing dates

- Details for you

- Details for a spouse, partner or beneficiary

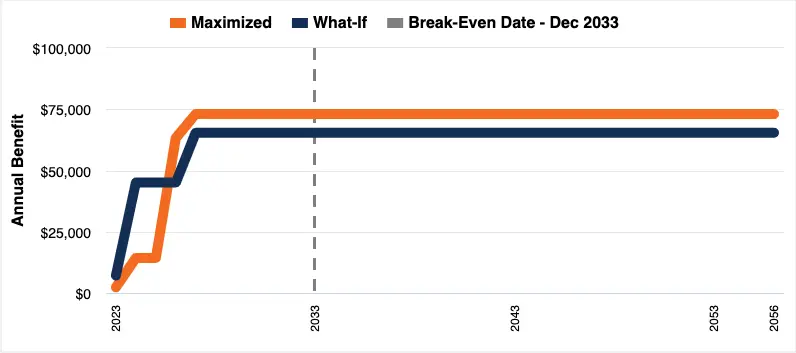

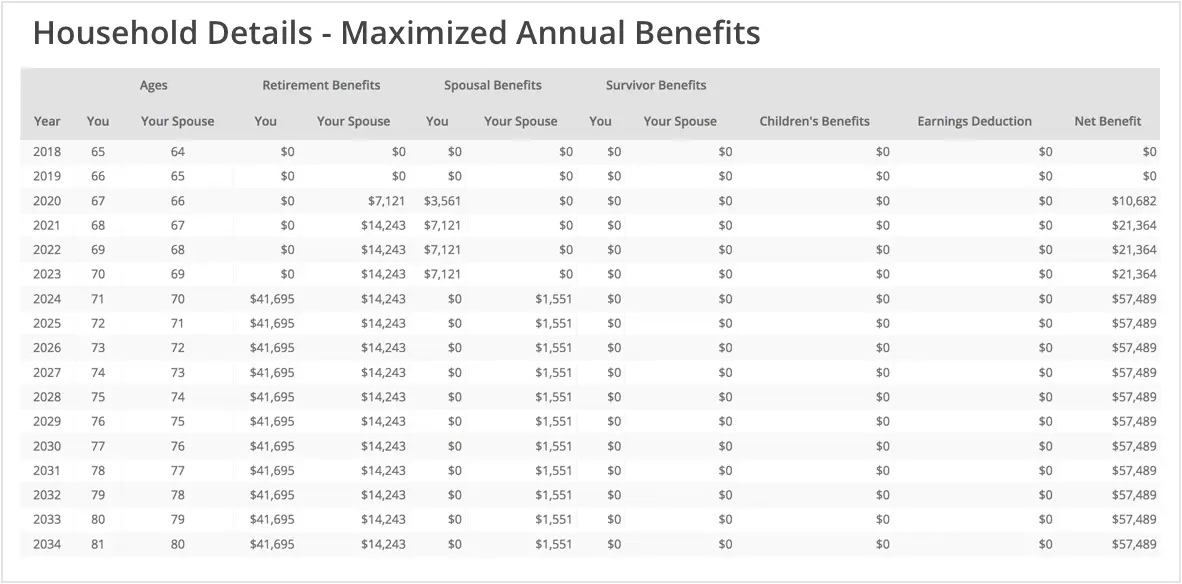

Detailed Reports Show Year-by-Year Benefits

View important detail on benefit amounts received each year under both your “what-if” strategy and the Maximized Plan, including when your Maximized Plan benefits break even with your “what-if” benefits.

Easy to Use. Try Unlimited What-If Scenarios.

- Used successfully by thousands of customers

- Step-by-step guidance––enter data in minutes

- Find maximized strategy to increase lifetime benefits

- Try unlimited what-ifs

- retirement dates

- earnings projections

- maximum ages

- filing dates

- benefit cuts

- See detailed results online or download and print